Halfpoint Images | Moment | Getty Images

Are you aware that some retirement savers can still snag an extra tax incentive for 2023? Surprisingly, most eligible filers don’t claim it, according to the IRS.

Here at Extreme Investor Network, we want to help you maximize your savings potential with the retirement savings contribution credit, also known as the “saver’s credit.” This credit can assist low- to moderate-income filers in offsetting part of the funds added to an individual retirement account, 401(k) plan, or other workplace plan.

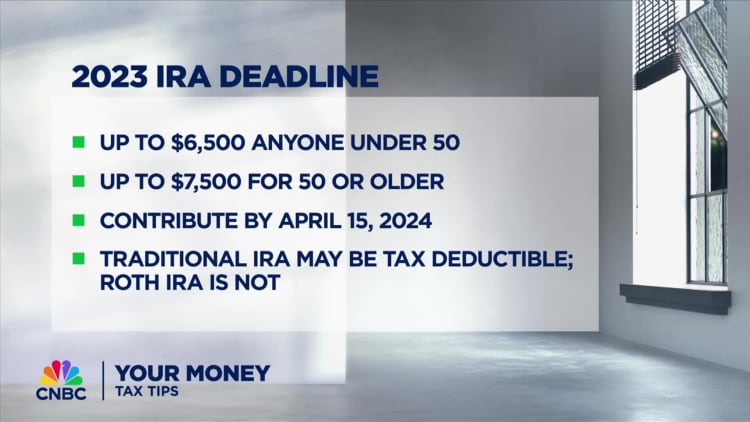

Did you know that you can still make a 2023 contribution to an IRA before the April 15 filing deadline to “earn a special tax credit,” as stated by the IRS?

How the saver’s credit works

With the saver’s credit, you can claim as much as 50% of retirement contributions up to $2,000 for single filers or $4,000 for married couples filing jointly, for maximum credits of $1,000 or $2,000, respectively.

This tax break offers a dollar-for-dollar reduction of levies owed, potentially reducing your tax bill or increasing your refund.

However, there are income limitations to consider. For 2023, your adjusted gross income can’t exceed $21,750 for single filers or $43,500 for married couples to qualify for the 50% credit.

Still, if you qualify for the saver’s credit, you could benefit from multiple tax breaks for a last-minute deposit, including deductions for pretax IRA contributions or tax-free growth for Roth IRA deposits.

Why few filers claim the saver’s credit

Despite the incentive, only 5.7% of taxpayers claimed the saver’s credit for tax year 2021, according to IRS estimates. There are reasons for this low percentage, experts say.

Many low-earning Americans have little or no tax burden, and since the saver’s credit isn’t refundable, they can’t benefit from the credit without owing taxes.

If you don’t have much of a tax burden, or any tax liability at all, the value of the credit is extremely limited or potentially zero.

Emerson Sprick, Associate Director for the Bipartisan Policy Center’s Economic Policy Program

Despite the benefits of the saver’s credit, many individuals are not aware of its existence. According to a recent survey from the Transamerica Center for Retirement Studies, fewer than half of U.S. workers are aware of the saver’s credit.

Furthermore, even if someone is aware of the credit and has a tax liability, they still need to have enough funds to save, as highlighted by Emerson Sprick, an expert in economic policy.

In 2027, the saver’s credit is set to convert to a saver’s match from the federal government, which could potentially address some of the current restrictions. However, barriers to retirement savings still exist.

Here at Extreme Investor Network, we believe that the most effective way to encourage individuals to save for retirement is through employer-sponsored retirement plans with automatic contributions. While access to these plans has improved, many Americans still do not have access to a workplace retirement plan.