Two weeks ago, just when everyone thought that he couldn’t turn any more bearish, BofA’s chief investment strategist Michael Hartnett, Wall Street’s biggest bear who is by extension has also emerged as the most accurate sell-side analyst (the average S&P price target of his peers was around 5,000 when he first correctly warned a recession and bear market were coming), stunned everyone when he told readers that according to his calculations, the bear market we are in now – and which is official as of today – would end in October with the S&P sliding to 3,000.

Fast forward to today, when in his latest must-read Flow Show note, Hartnett takes a well-deserved victory lap having steamrolled such “strategist” competitors as Marko Kolanovic and David Kostin, and writes that the heard on the street phrase this week is that “3,600 is the new bull case.”

While there is nothing materially new in Hartnett’s latest weekly Flow Show note, the BofA Chief Investment Strategist as always recaps the “biggest picture” best, by once again emphasizing the three shocks of 2022 which for now at least define “the story” of 2022, to wit:

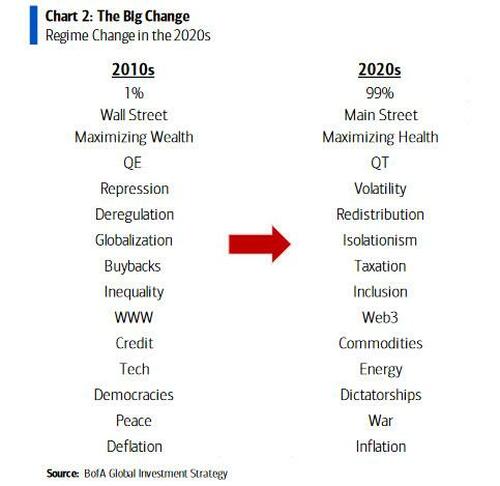

the story of 2022 is “inflation shock = rates shock = recession shock”; the larger story of the 2020s is regime change – higher inflation, higher rates, higher volatility, & lower asset valuations, driven by trends in society (inequality), politics (populism/progressivism), geopolitics (war), environment (net-zero), economy (de-globalization), demographics (China population decline), all inflationary, all favor cash, commodities, real assets, volatility, small cap, all damage bonds, credit, private equity, tech stocks.

Hartnett then takes us through the usual weekly fund flows, where we find widespread redemptions across every asset class: starting with $1.4bn from gold, through $5.2bn from equities, another $7.6bn from cash, and ending with $12.3bn from bonds.

That said, the pain for credit is far greater than stocks – for every $100 of inflow to IG/HY/EM debt since Apr’20, $27 has been redeemed; for every $100 of inflow to global equities since Jan’21, only $4 has been redeemed.

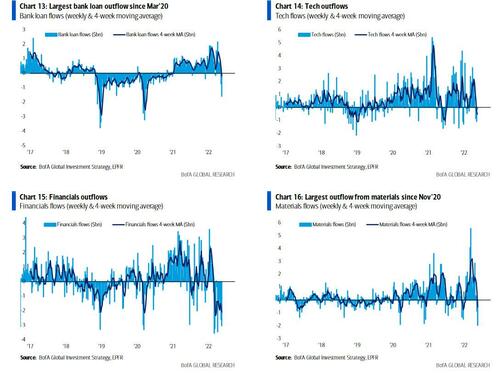

In this context, and in light of the relentless selling, it is not surprising that last week saw the largest EM debt outflow since Mar’20 ($6.1bn), the largest HY bond outflow in 14 weeks ($4.3bn), the largest bank loan outflow since Mar’20 ($1.6bn); outflows tech & financials, largest outflow from energy since Sep’16 ($1.7bn), largest outflow from materials since Oct’14 ($2.0bn) and so on.

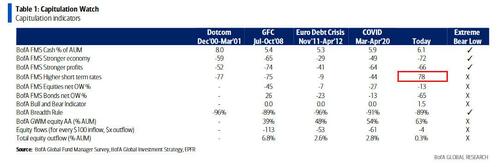

Does that mean that capitulation is here? Alas, for the second week in a row, the answer is no. As Hartnett shows in the “Capitulation watch” table below, while FMS cash/macro + breadth = capitulation & BofA Bull & Bear <2; but institutional & private client AA + equity flows are not at capitulation lows; and of course, true capitulation = Fed capitulation, and systemic event & unemployment rate rise required first.

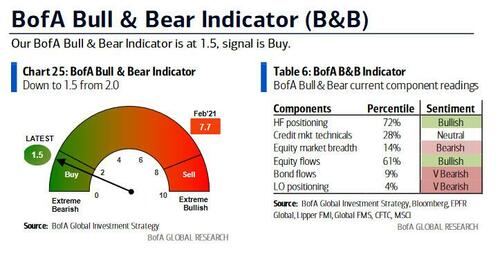

And while capitulation may not be here yet, it’s worth pointing out that the BofA Bull and Bear Indicator, and of the most accurate forward-looking tests for when to buy, has tumbled to 1.5 from 2.0 in unambiguous contrarian buy territory on redemptions in developed market stocks & HY/EM debt, deteriorating equity breadth, and bearish May FMS.

Doubling down on the bull case, the BofA Global Breadth Rule is also a contrarian “buy” signal level (i.e. >88% of equity indices trading <50d & 200dma). Alas, despite these tactical “green lights” to go long risk, Hartnett is still skeptical that this is the time to buy, and writes that his bottom “tactical” line is that while the tape remains very vulnerable to a bear market rally, he would still “sell-any-rips”.

Not only that, but Hartnett also makes it clear that he would be selling some of the big winners of the current rotation. Showing a chart of the Saudi stock market which is down >10% in the past 10 days, Hartnett warns that we may have reached a peaky oil price; as a result, resources, REITs, Big Tech, and the US dollar are all the pre-recession vulnerable longs.

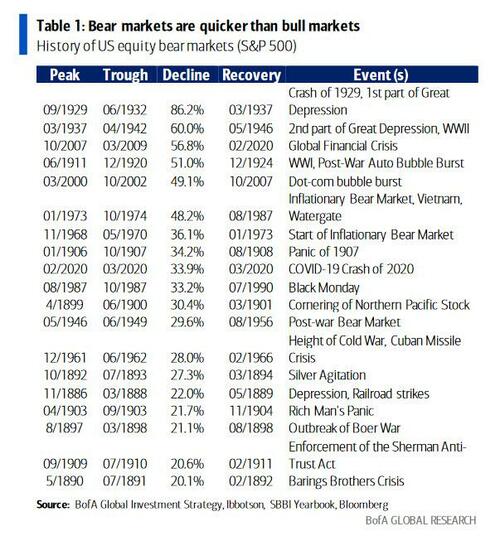

Next, Hartnett walks us through a couple of history lessons, the first one is a reminder of what he said two weeks ago when he calculated that there have been 19 US bear markets past 140 years – the average price decline is 37.3% and the average duration is 289 days.

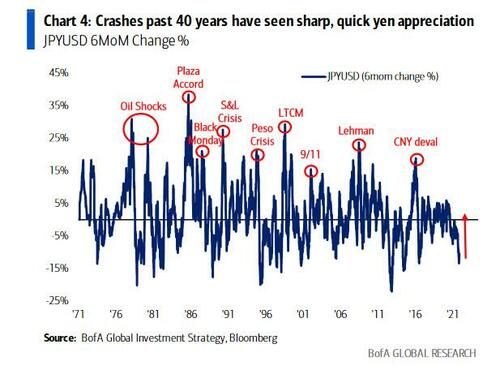

If this is repeated today, the bear market ends Oct 19th, 2022 with S&P500 at 3000, Nasdaq at 10000; How to hedge this bear market? According to the BofA strategist, do so via the Japanese yen and Swiss franc as pretty much every Wall St crash past 40 years has seen sharp, quick yen appreciation.

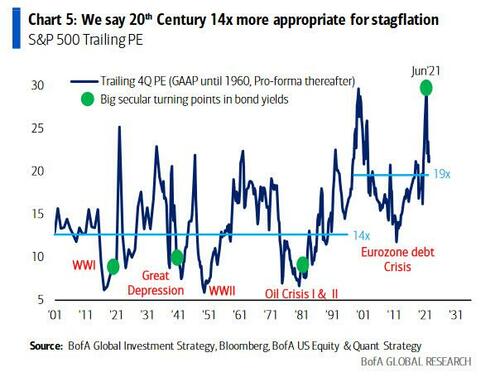

Hartnett also shares a second history lesson: when EPS/GDP forecasts head lower, the debate shifts to what is the correct multiple; and while some say 21st Century multiple of 19x is still appropriate, Hartnett counters that a 20th Century multiple of 14x is more appropriate for stagflation.

Hartnett concludes by taking a divergent dive into what the two market camps are saying now, starting with the (slightly shocked) bulls, who just saw the S&P enter a bear market only to rebound less than an hour later:

Bulls say: feral, fearful, dystopian price-action – this is what bear markets are, and the tape shows big damage already; bulls can say “inflation shock” largely priced-in, “rates shock” too, and once “recession shock” discounted lows will be set. According to Hartnett, the key for bulls now is JOLTs data (where the most recent job openings hit a record 11.5mn). This needs to pullback below 10 million to induce bullish peak wages, peak yields, and peak dollar narrative.

To all this, the Bears counter that unanticipated cyclical risks are…

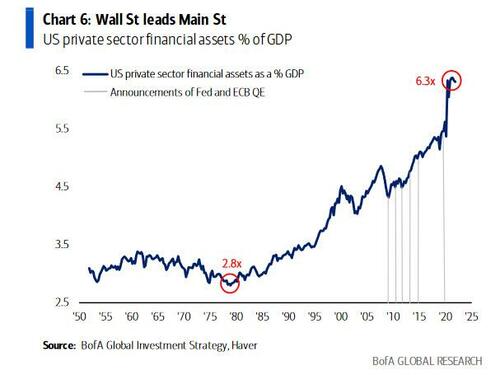

Wall St leads Main St: Wall Street assets are 6.3x greater than US GDP as seen in 2020 – and as the Fed clearly realizes – the quickest route to deep recession is via Wall St crash (and vice-versa).

Recession: housing & labor markets only just at inflection points…see US purchase loan applications (Chart 7), see tech & retail layoffs (retail = 12% job gains past 2 years, leisure & hospitality 33% – Chart 8)…

… and higher unemployment = social unrest; meanwhile China’s house prices are negative once again (Chart 9),

- Policy paralysis: inflation hinders Fed reaction function, polarization hinders fiscal policy reaction function in a crisis, recession,

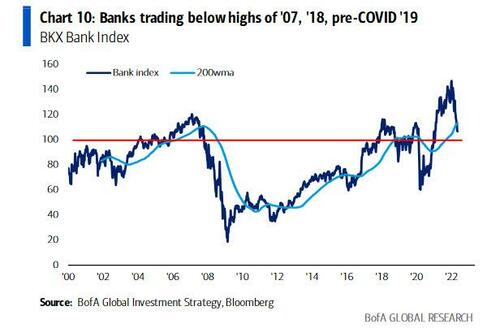

- Banks are arguably the safest part of the financial system yet the BKX index trades below highs of ’07, ’18, pre-COVID ’19…

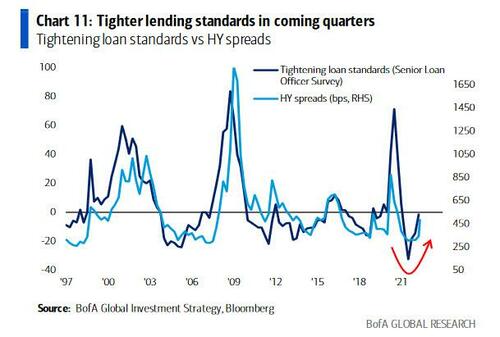

… break below 100 would scream recession and/or credit event, tighter lending standards in coming quarters.

Or another way of putting all this is who will be this recession’s deflation-triggering Lehman?

- Credit events: Hartnett still thinks $18tn of negatively-yielding debt to $2tn in 9 months means a high risk of liquidation & deleveraging & default; And indeed, the leveraged loan market is cracking, with systemic risk from bond/stock/real estate deleveraging in risk parity (RPAR), private equity (PSP) high, PE exposure to syndicated loans high, sovereign wealth funds, credit events in speculative tech, shadow banking, US consumer buy now, pay later models, European credit/banks/housing, Emerging Markets, zombie corporations, and so on… and yet the Fed has not even begun QT…