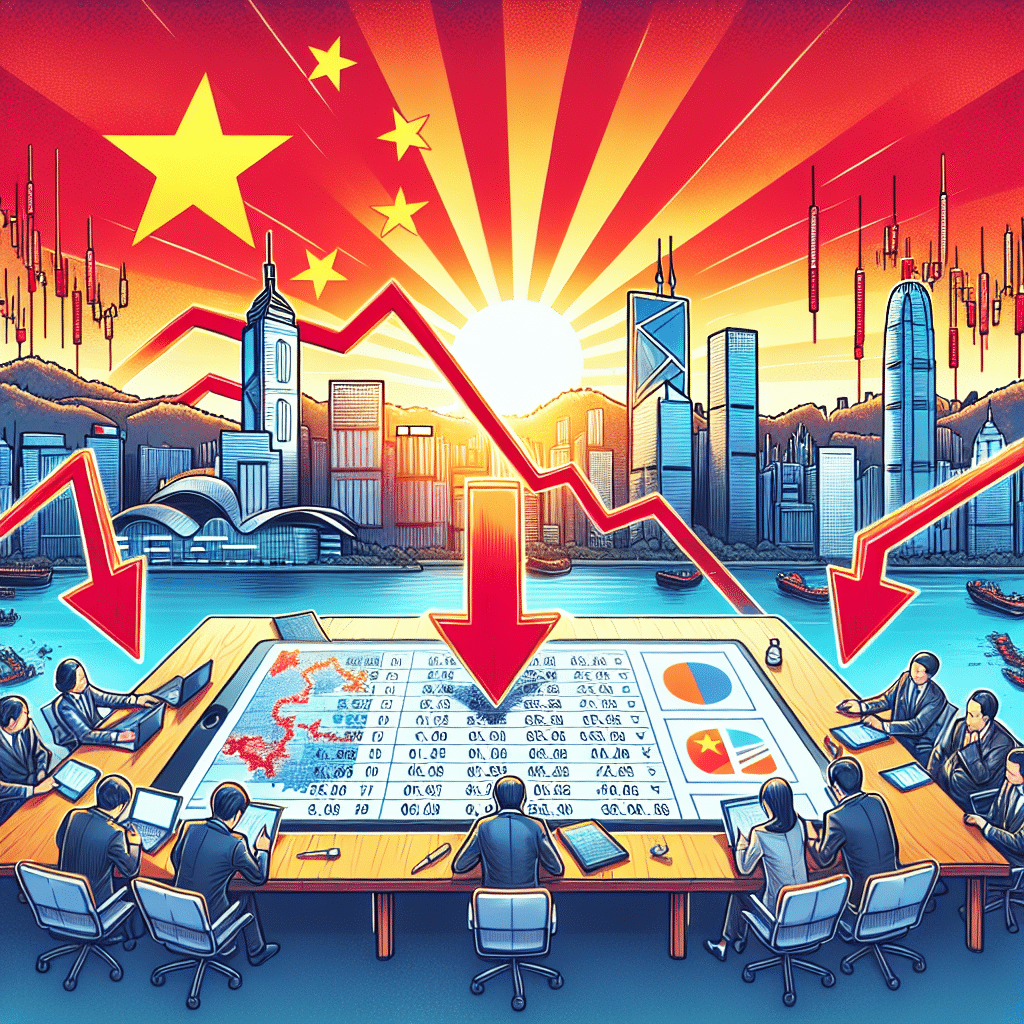

China Faces Growing Deflation Threat Amid Slumping Trade Data — What Hang Seng’s Unexpected Rally Means for Investors

China’s Export Slowdown: A Harbinger of Deflationary Pressures and What Investors Must Do Now

China’s recent trade data has sent a clear signal to global markets: the export engine is losing steam, and with it, deflationary pressures are mounting. While the Manufacturing PMI hinted at improving domestic demand, the export figures tell a more sobering story. August saw exports rise by only 4.4% year-over-year, a sharp deceleration from July’s 7.2%, with shipments to the US plummeting a staggering 33%. This divergence between domestic manufacturing optimism and external demand weakening is a red flag for investors globally.

The Deflation Domino: Why Export Weakness Matters

The slowdown in exports isn’t just about China’s trade balance; it’s a signal of intensifying global competition and potential price wars. When external demand wanes, Chinese exporters are pressured to lower prices to maintain market share, passing cost savings onto consumers worldwide. This dynamic could exacerbate deflationary pressures, especially in economies heavily reliant on Chinese imports.

A key factor to watch is the ongoing US-China trade relationship. While a potential trade agreement reducing tariffs could reignite demand and stoke inflationary pressures, the current trajectory of rising US levies and geopolitical tensions suggests deflationary forces may dominate in the near term. This is a nuanced battleground: on one side, tariff relief could boost prices and demand; on the other, escalating trade friction tightens the screws on Chinese exporters, pushing prices down.

Beijing’s Balancing Act: Stimulus on the Horizon

China’s policymakers are acutely aware of these risks. Despite weak trade data, Beijing has pledged stimulus measures aimed at shoring up the housing market, boosting employment, and encouraging domestic consumption. These moves are designed to offset external demand shortfalls by invigorating internal economic engines.

Upcoming economic data releases—retail sales, industrial production, and unemployment figures—will be critical. Should these numbers disappoint, expect Beijing to accelerate stimulus efforts ahead of the Politburo meeting later this month. This proactive stance is a double-edged sword: while stimulus can buoy markets and consumption, it may also signal deeper economic fragility.

Market Reactions and What Investors Should Watch

The immediate market response to China’s mixed data has been muted but telling. The Hang Seng Index edged up 0.60%, reflecting cautious optimism fueled by stimulus hopes. Mainland indices like the CSI 300 and Shanghai Composite showed minimal movement, underscoring investor uncertainty.

For investors, this environment demands a recalibrated strategy:

- Diversify Exposure: With Chinese exports slowing and deflationary pressures rising, diversify portfolios beyond China-centric equities and commodities vulnerable to price wars.

- Focus on Domestic Consumption Plays: Beijing’s stimulus targeting domestic demand suggests opportunities in sectors like consumer staples, real estate, and services that benefit from policy support.

- Monitor US-China Trade Developments: Trade policy remains a key variable. Any thaw in relations could quickly shift inflation dynamics, impacting global supply chains and commodity prices.

- Watch Inflation Indicators Globally: As Chinese deflationary pressures mount, global inflation trends may diverge, creating arbitrage opportunities in fixed income and currency markets.

Unique Insight: The Ripple Effect on Emerging Markets

An often-overlooked consequence of China’s export slowdown is its impact on emerging markets (EM). Many EM economies are tightly linked to Chinese demand, either as suppliers of raw materials or as export destinations themselves. According to the IMF, over 30% of emerging market export revenues are tied to China. As Chinese demand softens, expect a ripple effect causing slower growth and increased currency volatility in these regions. Investors should consider hedging EM exposure or selectively overweighting countries with diversified trade partners.

What’s Next?

The next few weeks are pivotal. Watch for:

- Beijing’s stimulus announcements and their scope.

- August economic data releases for signs of domestic resilience or further weakness.

- US-China trade talks for any breakthroughs or escalations.

- Inflation trends in major economies as a counterbalance to China’s deflationary signals.

In conclusion, China’s export slowdown is more than a headline—it’s a signal flare for investors to rethink exposure and strategies amid rising deflationary pressures and geopolitical uncertainty. Staying agile, informed, and diversified is the best defense and offense in this evolving landscape.

Sources:

- Bloomberg: China Trade Data and Market Reactions

- IMF: Emerging Markets and China Trade Linkages

- Reuters: Beijing Stimulus Measures and Economic Outlook

Stay tuned with Extreme Investor Network for the latest insights and actionable strategies as this critical story unfolds.

Source: China Deflation Risks Intensify as Trade Data Weakens; Hang Seng Index Gains