Zoltan Pozsar Warned Us

In a post about a month ago (The Fed Isn’t Your Friend), we wrote about Zoltan Pozsar’s warning that the Fed’s helicopters were going to be dropping “financial” napalm on the stock market.

In a nutshell, Pozsar’s argument was that the Fed needed a reverse wealth effect (a poverty effect?) to reign in inflation:

The Fed Needs Stocks to Fall

This is what they actually mean when they talk about the need to “tighten financial conditions”. In support of this claim, Poszar cites a Bloomberg column by his former boss, former NY Fed President Bill Dudley, ominously titled, “If Stocks Don’t Fall, The Fed Needs To Force Them”. The Fed also needs real estate to fall and (more controversially), unemployment to rise, per Poszar.

This all makes sense intuitively if you think about it. You just need to invert the status quo since the Fed last conquered inflation in the early ’80s under Paul Volker. After that, and up until the COVID lockdowns, the Fed’s primary concern was deflation, rather than inflation. In a deflationary environment, consumers are hesitant to spend, because they’re waiting for prices to drop further. That, in turn, can fuel more deflation. One way to encourage consumers to spend is through the wealth effect. If they see their IRAs and 401(k)s balances rise, they feel richer and are more inclined to spend money.

If rising stocks make consumers want to spend more, heating up inflation with their demand, what would make them want to spend less, cooling inflation down? Correctamundo, readers: falling stocks is the answer.

Positioning In Response To Poszar’s Warning

At the time, we noted how our system was positioned in response to Poszar’s warning:

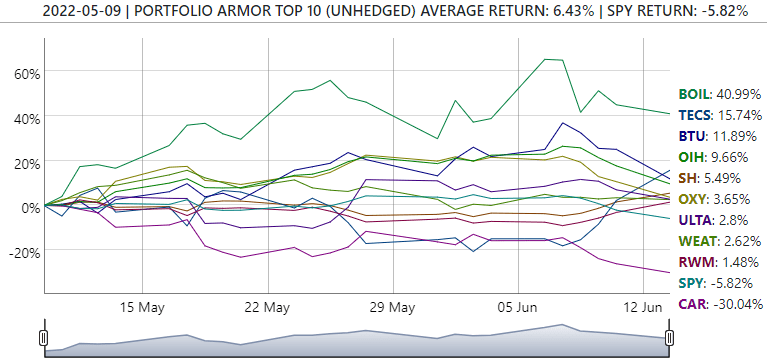

If Poszar is right, it would seem you’d want to be short stocks now, with the possible exception of companies benefiting from demand-side inflation like oil majors. With that in mind, take a look at Portfolio Armor’s top ten names from May 9th.

Screen capture via Portfolio Armor on 5/9/2022.

As regular readers know, our system doesn’t consider the macro picture when selecting its top names. Instead, it gauges stock and options market sentiment to estimate which securities are likely to perform the best over the next six months. Nevertheless, that bottoms-up approach often paints a clear picture, and the one it painted last Monday seems fairly well aligned with Poszar’s thesis: Three of our top ten names were bets against stocks: the ProShares Short S&P500 (SH), Direxion Daily Technology Bear 3X Shares (TECS), and ProShares Short Russell2000 (RWM). Five of the other seven top ten names were in the commodity space: ProShares Ultra Bloomberg Natural Gas (BOIL), Teucrium Wheat Fund (WEAT), VanEck Vectors Oil Services (OIH), Occidental Petroleum Corp. (OXY), and Peabody Energy Corp. (BTU).

How That Worked Out After Monday’s Crash

Here’s how our top ten names from May 9th have done since, as of Monday’s close. On average, they’re up 6.43%, while the SPDR S&P 500 Trust ETF (SPY) is down 5.82%.

Note that our top five performers from May 9th include three energy names (BOIL, BTU, and OIH) and two bets against stocks (TECS and SH). BOIL tumbled about 33% Tuesday on the Freeport LNG news; had that happened yesterday, the chart above would have shown our top ten names from May 9th outperforming SPY by about 9% instead of by about 12.85%.

BOIL’s drop today illustrates though why we suggest readers consider hedging, particularly when it comes to leveraged ETFs such as BOIL and TECS. As a reminder, you can use our website or our iPhone app to scan for optimal hedges on any of our top names.

Where We Go From Here

In his warning last month, Pozsar said he wouldn’t give a price target for the S&P 500, but he did offer this guidance:

At 4,000, the Fed does not seem content, and in the grand scheme of things, this is where the Fed would change its tune if it would still be writing a put. At 3,500, we would have lost all of the post -pandemic gain s in market wealth, but that level for stocks still feels like a put option, just with a lower strike price. At 2,500, we would lose not only all of the post -pandemic gain s, but would eat into some of the pre -pandemic gains too. And if something indeed happened to the supply of labor post -pandemic (and some of that is wealth related), then to cool price pressures, maybe a pre -pandemic wealth level is appropriate indeed.

Given that we closed at 3,749.63 on Monday, we could have a bit more to fall.